Investment Thesis: Netflix

fNetflix (NASDAQ: NFLX) is the world’s leading subscription streaming platform, serving over 260 million members across more than 190 countries. Founded in 1997 as a DVD-by-mail service, Netflix has evolved into a global entertainment powerhouse, producing and distributing original films, series, documentaries, and live programming. Through its direct-to-consumer model, data-driven content strategy, and global production scale, the company has reshaped how audiences consume media and how studios monetize content. The investment case for Netflix centers on its global scale, pricing power, and expanding monetization levers. As traditional linear television declines and streaming becomes the primary mode of content consumption, Netflix benefits from its strong brand, diversified content slate, and recurring subscription revenue model. The company has also introduced advertising-supported tiers and cracked down on password sharing to drive incremental revenue and improve margins. Supported by improving free cash flow generation, disciplined content spending, and a growing international footprint, Netflix represents a scaled digital platform positioned to compound earnings over the long term.

This recommendation is just a start. The next step is to do your due diligence process, which will then help you make the investment decision. We strongly advise investors to do a thorough analysis of the recommendation and understand the soundness of the business before investing in this company. Also, please consult your investment advisor before making a decision.

Business Profile (NASDAQ: NFLX)

Netflix, headquartered in Los Gatos, California, is the world’s largest subscription-based streaming entertainment service. Founded in 1997, the company transitioned from a DVD-by-mail rental business into a global direct-to-consumer streaming platform, now operating in more than 190 countries. Netflix offers a vast library of licensed and original content, including films, scripted and unscripted series, documentaries, anime, stand-up specials, and select live programming.

Netflix is evolving from a streaming pioneer into a global, profit-driven entertainment platform built for long-term growth.

From disrupting video rental stores in the early 2000s to reshaping global television distribution, Netflix has built a scalable digital platform powered by data, technology, and storytelling. Its core business model is subscription-based, with multiple pricing tiers, including a lower-cost advertising-supported plan. This structure provides recurring revenue, global reach, and flexibility to serve diverse income segments across developed and emerging markets.

The company operates a vertically integrated content ecosystem, spanning content acquisition, production, distribution, and personalized recommendation algorithms. Netflix invests heavily in original programming under the “Netflix Originals” banner, producing localized content across regions such as North America, Europe, Latin America, and Asia-Pacific. Its global production infrastructure allows it to create culturally relevant content while distributing hits worldwide, strengthening both engagement and retention.

Unlike traditional media networks, Netflix distributes content exclusively through its own platform, accessible via smart TVs, smartphones, tablets, gaming consoles, and web browsers. This direct relationship with subscribers provides valuable viewing data, enabling better content commissioning decisions and more efficient marketing spend.

As of FY25, Netflix generates revenue primarily from subscription fees and a growing advertising segment. With expanding monetization levers such as ad-tier scaling, paid sharing initiatives, and selective price increases, the company continues to evolve from a high-growth disruptor into a mature, cash-generative global entertainment platform.

Story: From DVD Disruptor to Global Streaming Powerhouse

Netflix’s story is one of constant reinvention.

1997 to 2006: The DVD Era

Netflix was founded in 1997 by Reed Hastings and Marc Randolph after testing whether a DVD could survive being mailed. When it did, the idea for a DVD-by-mail rental service was born. At the time, Blockbuster dominated through physical stores and late fees. Netflix differentiated itself with convenience and a customer-friendly subscription model.

In 1999, Netflix introduced unlimited DVD rentals with no due dates or late fees, shifting from transaction-based rentals to recurring subscription revenue. In 2000, it launched a personalized recommendation system based on member ratings, embedding data-driven decision-making early into its model.

The company went public in 2002 at $1 per share under NASDAQ ticker NFLX. Membership surpassed 1 million by 2003 and reached 5 million by 2005, establishing Netflix as a credible national competitor to brick-and-mortar chains.

This era was defined not just by DVD logistics, but by subscription economics and personalization — foundations that would later power its transition into global streaming.

2007 to 2012: The Streaming Pivot

In 2007, Netflix introduced streaming, allowing members to instantly watch series and films online. What began as a complementary feature to its DVD-by-mail service would soon redefine the company’s future. Broadband penetration was rising, device connectivity was improving, and consumer behavior was shifting toward on-demand digital viewing. Netflix recognized early that distribution was migrating from physical media to the internet.

Device integration became a critical enabler. In 2008, Netflix partnered with consumer electronics brands to bring streaming to the Xbox 360, Blu-ray players, and TV set-top boxes. Rather than requiring users to watch on a computer, Netflix embedded itself directly into the living room. This distribution strategy accelerated in 2009 as partnerships expanded to internet-connected TVs. That same year, membership surpassed 10 million, and Netflix awarded the $1 million Netflix Prize to the team BellKor’s Pragmatic Chaos for improving recommendation accuracy by 10 percent. The publication of the Netflix Culture Deck further clarified the company’s high-performance philosophy and long-term ambition.

International expansion followed. In 2010, Netflix entered Canada, marking its first move outside the United States, and streaming launched on mobile devices, anticipating the shift toward smartphone viewing. In 2011, the service expanded into Latin America and the Caribbean. The first Netflix button appeared on remote controls, reducing friction between the viewer and the platform. The company also introduced its first parental controls on streaming, signaling a growing family audience and product maturity.

By 2012, Netflix had entered parts of Europe, cementing its transition from a domestic DVD distributor into a global streaming platform. Although its streaming library initially relied heavily on licensed studio content, management increasingly understood the strategic vulnerability of dependence on third-party providers. The groundwork for original content investment was already being laid.

The 2007 to 2012 period was not just a product evolution. It was a structural pivot. Netflix moved from physical logistics to digital distribution, from domestic scale to global ambition, and from rental economics to recurring subscription streaming. The foundation for its next phase of growth was firmly in place.

2013 to 2019: The Originals Revolution

Netflix’s shift from distributor to global studio began in 2013 with its first major slate of originals, including House of Cards, Hemlock Grove, Arrested Development, and Orange Is the New Black. Rather than relying solely on licensed content, Netflix chose to own premium programming. The strategy paid off quickly, with House of Cards winning three Primetime Emmy Awards, marking the first major wins for a streaming service.

Product innovation supported this content push. Features like Profiles and “My List” enhanced personalization, while a redesigned TV homepage improved discovery. Expansion accelerated across Europe and Asia, membership surpassed 50 million in 2014 and 100 million by 2017, and streaming quality advanced with 4K support. Netflix also launched its first original film (Beasts of No Nation) and first non-English original series (Club de Cuervos), signaling global creative ambition.

In 2016, Netflix expanded into 130 new countries, bringing the service to more than 190 markets. Offline downloads strengthened mobile engagement. By 2018, Netflix was the most-nominated studio at the Emmys®, reflecting both critical and commercial success.

During this period, global hits such as Stranger Things and La Casa de Papel validated the power of local-language content with worldwide appeal. By the end of the decade, membership exceeded 150 million, and Netflix had firmly established itself as a fully integrated global entertainment studio built on data, technology, and owned intellectual property.

2020 to 2021: Pandemic Surge and Platform Deepening

The COVID-19 pandemic in 2020 accelerated global streaming demand as lockdowns kept audiences at home. Netflix saw a surge in subscriber growth and engagement, driven by breakout titles such as The Queen’s Gambit and the global hit Squid Game. The company became the most-nominated studio at both the Academy Awards® and the Emmys®, reinforcing its growing creative credibility.

Product enhancements strengthened engagement. The launch of Top 10 lists introduced visibility into trending content, blending personalization with social proof. Despite production delays caused by global shutdowns, Netflix supported the creative community through a Hardship Fund and committed two percent of its cash holdings toward community impact investments.

In 2021, membership surpassed 200 million. Netflix expanded into mobile gaming, introduced Tudum to deepen fan engagement, and committed to reaching net-zero greenhouse gas emissions by the end of 2022.

Together, these years combined extraordinary demand growth with strategic expansion, reinforcing Netflix’s global scale while broadening its platform beyond traditional streaming.

2022: Reset and Strategic Shift

In 2022, Netflix hit its first major inflection point, reporting net subscriber losses after years of uninterrupted growth. Competition intensified from Disney+, Amazon Prime Video, and HBO Max, prompting investors to question whether streaming growth had peaked.

Management responded with a decisive reset. Netflix launched a lower-priced, ad-supported tier in 12 countries, expanding its addressable market and introducing a new advertising revenue stream. It also implemented paid sharing initiatives to convert password borrowers into paying members. At the same time, cost discipline increased, with more deliberate content spending and tighter capital allocation. The focus shifted from growth at any cost to sustainable margin and free cash flow expansion.

Beyond the platform, Netflix strengthened its brand ecosystem with Netflix Is a Joke: The Festival, a large-scale live event in Los Angeles spanning 11 days and 295 shows.

2022 marked a strategic pivot. Netflix transitioned from expansion-driven momentum to monetization discipline, laying the groundwork for improved margins and long-term profitability.

2023 to 2025: Monetization, Live Expansion, and Margin Discipline

From 2023 onward, Netflix shifted firmly into a monetization-driven phase. Subscriber growth stabilized, the ad-supported tier gained traction, and paid sharing initiatives converted non-paying users into members. Revenue growth began to outpace content spending, expanding operating margins and strengthening free cash flow.

At the same time, Netflix expanded beyond traditional on-demand streaming. In 2023, it launched its first major live global stream with Chris Rock: Selective Outrage and extended its IP into physical entertainment with Stranger Things: The First Shadow in London’s West End. Product engagement deepened with “My Netflix,” a centralized in-app hub for personalization and discovery.

In 2024, live programming scaled with the Screen Actors Guild Awards, The Roast of Tom Brady, two Christmas Day NFL games, and the Jake Paul vs. Mike Tyson fight, which became the most-streamed sporting event in history. The “Moments” feature enhanced mobile engagement, and membership surpassed 300 million globally.

By 2025, Netflix became the home of WWE programming and introduced a redesigned TV interface to simplify discovery and improve user experience.

This period marked a strategic maturation. Netflix layered advertising, live events, sports rights, and product enhancements onto its subscription foundation, evolving into a scaled, cash-generative global platform with expanding margins and multiple monetization levers.

2026: A Scaled Global Entertainment Platform

As of February 2026, Netflix serves over 260 million members worldwide. It operates across nearly every major geography, with a diversified content portfolio spanning Hollywood blockbusters, regional productions, documentaries, animation, and live content.

From mailing DVDs in red envelopes to powering a global streaming ecosystem, Netflix’s journey reflects its willingness to disrupt itself before others could. Its story is not just about growth but about strategic adaptation in a rapidly evolving media landscape.

📌 Further Reading

- Netflix Annual Reports

https://ir.netflix.net/financials/annual-reports-and-proxies/default.aspx

Comprehensive overview of Netflix’s historical performance, strategy, risks, and long-term positioning. - 2025 Annual Report

https://s22.q4cdn.com/959853165/files/doc_financials/2025/ar/99482238-46b2-4d0d-b292-40e6781bdf03.pdf

Most recent full-year financials, strategic priorities, and management commentary. - Netflix Newsroom

https://about.netflix.com/en/news

Official announcements covering live programming, product launches, advertising rollout, and strategic initiatives.

Business Model

Netflix operates a subscription-based business model centered on recurring monthly revenue rather than title-specific monetization. Unlike traditional film studios or television networks that depend on the commercial success of individual releases, Netflix generates revenue from access to its entire content library. Subscribers pay for the platform as a whole, which reduces volatility tied to any single show or movie and creates a predictable cash flow.

Subscription-Led Revenue Structure

The foundation of Netflix’s model is its tiered membership system, which includes both ad-free and advertising-supported plans. This structure allows the company to serve different income segments across global markets while maintaining a steady stream of recurring revenue. Because revenue is tied to memberships rather than one-time transactions, the focus shifts from box office hits to sustained engagement and retention.

Content Monetized as a Portfolio

A defining feature of Netflix’s model is how it treats content assets. Licensed and internally produced content is capitalized and amortized over its estimated useful life, but it is monetized collectively rather than on a per-title basis. Management evaluates content in aggregate when assessing potential impairment. If events or changes in circumstances indicate that the expected usefulness of the content library has declined, or that fair value may be lower than unamortized cost, the portfolio is reviewed at a group level. To date, no material impairment events have been identified under this framework. Should such changes arise in the future, aggregated content assets would be written down to the lower of unamortized cost or fair value, and any abandoned content would be written off accordingly.

This portfolio-based approach reflects the reality of streaming economics. Subscriber value is driven not by a single blockbuster, but by a steady pipeline of diverse programming that keeps members engaged month after month.

Vertically Integrated Distribution

Netflix operates an integrated model that spans content commissioning, production, licensing, and global digital distribution. By delivering content exclusively through its own platform, the company eliminates traditional intermediaries and retains direct control over pricing, user experience, and data. This direct-to-consumer relationship provides granular insight into viewing behavior, which informs content investment decisions and improves marketing efficiency.

Evolving Monetization Levers

While subscriptions remain the core revenue driver, Netflix has expanded its monetization toolkit. The introduction of an advertising-supported tier opened a new revenue stream while attracting more price-sensitive consumers. Paid sharing initiatives have converted non-paying users into paying members, and selective price increases in mature markets have supported revenue growth and margin expansion. The company has also experimented with live programming and event-based content to broaden engagement.

Overall, Netflix’s business model combines recurring subscription revenue with portfolio-level content monetization and global digital distribution. Its scale allows it to invest heavily in content while spreading risk across a vast and diverse library, positioning the platform as a durable, cash-generative entertainment ecosystem.

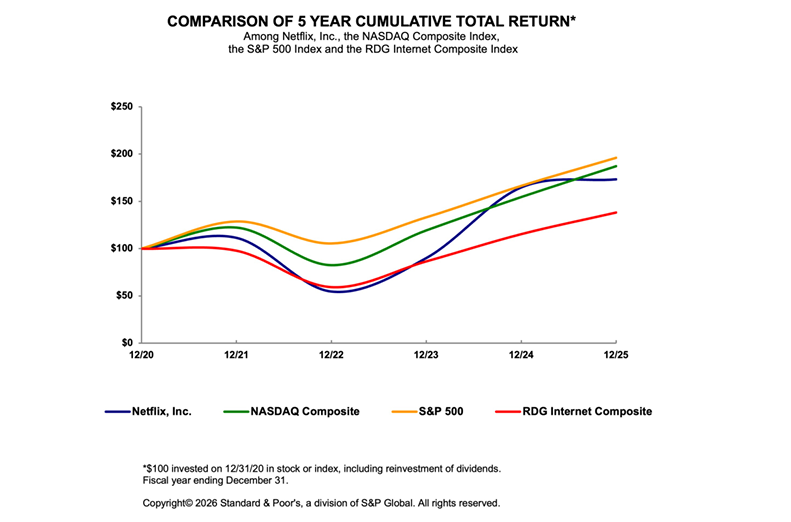

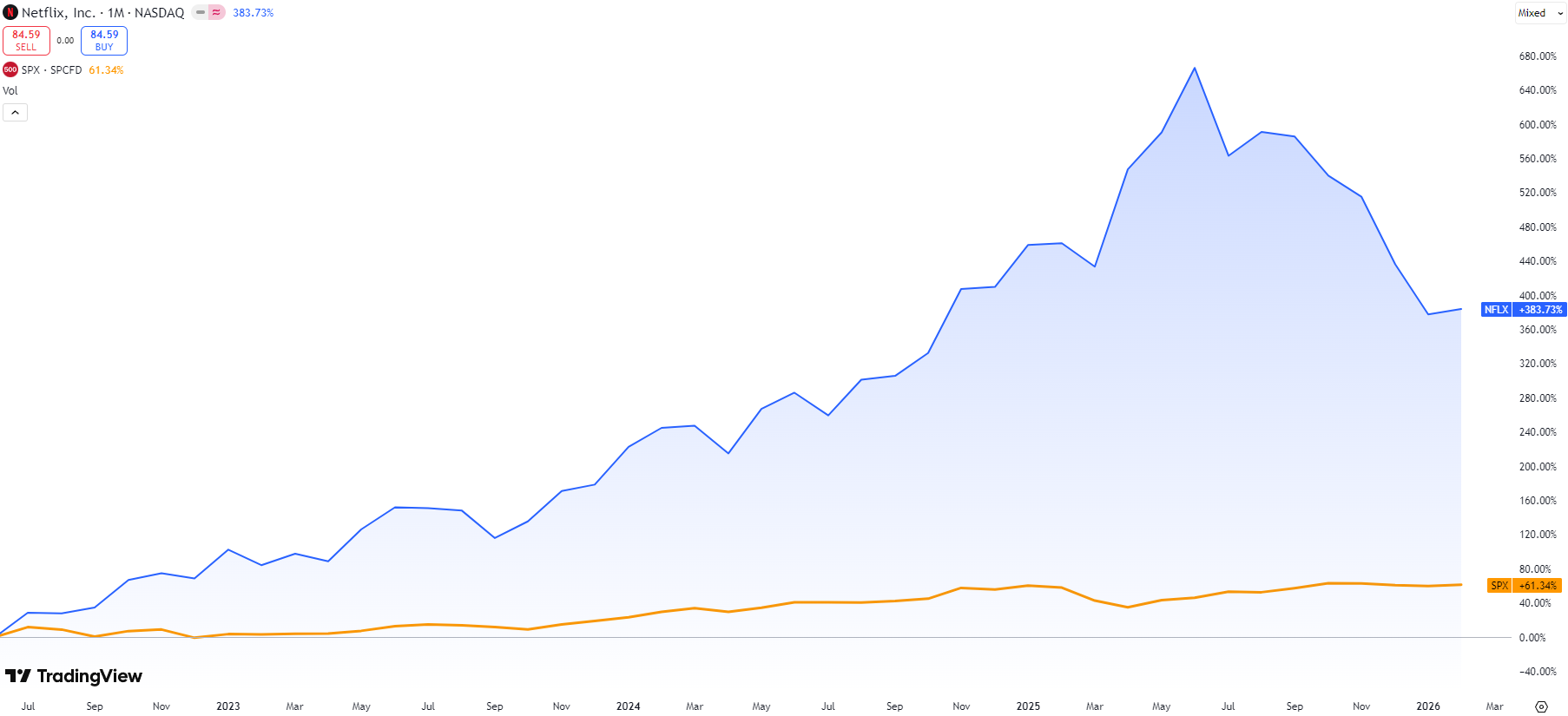

Market Performance and Shareholder Returns

How has the market rewarded Netflix’s evolution from DVD disruptor to global streaming powerhouse?

The chart below compares the five-year cumulative total return of Netflix against the NASDAQ Composite, the S&P 500, and the RDG Internet Composite Index. It reflects what would have happened if an investor placed $100 into each at the end of 2020 and reinvested dividends.

Over this period, Netflix’s journey was far from smooth. The stock experienced a sharp drawdown in 2022 as subscriber growth stalled and competition intensified. Market sentiment shifted quickly, reminding investors that even category leaders are not immune to execution risk.

However, as management recalibrated strategy through advertising, paid sharing, and tighter cost discipline, growth stabilized and profitability improved. The recovery that followed demonstrates how quickly high-quality digital platforms can re-rate when fundamentals strengthen.

For long-term investors, the key lesson is not just the total return, but the volatility required to earn it. Netflix has proven capable of compounding value, but only for shareholders willing to endure meaningful swings along the way.

Financial Performance

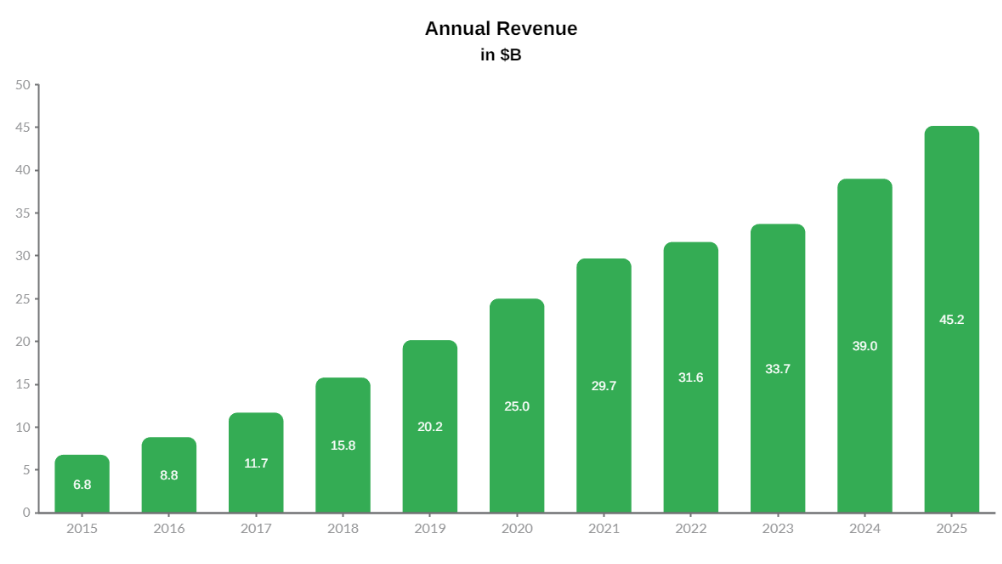

Over the past decade, Netflix has delivered substantial top-line expansion, reflecting its transformation from a U.S.-centric streaming service into a scaled global entertainment platform.

Revenue Growth: From Expansion to Optimization

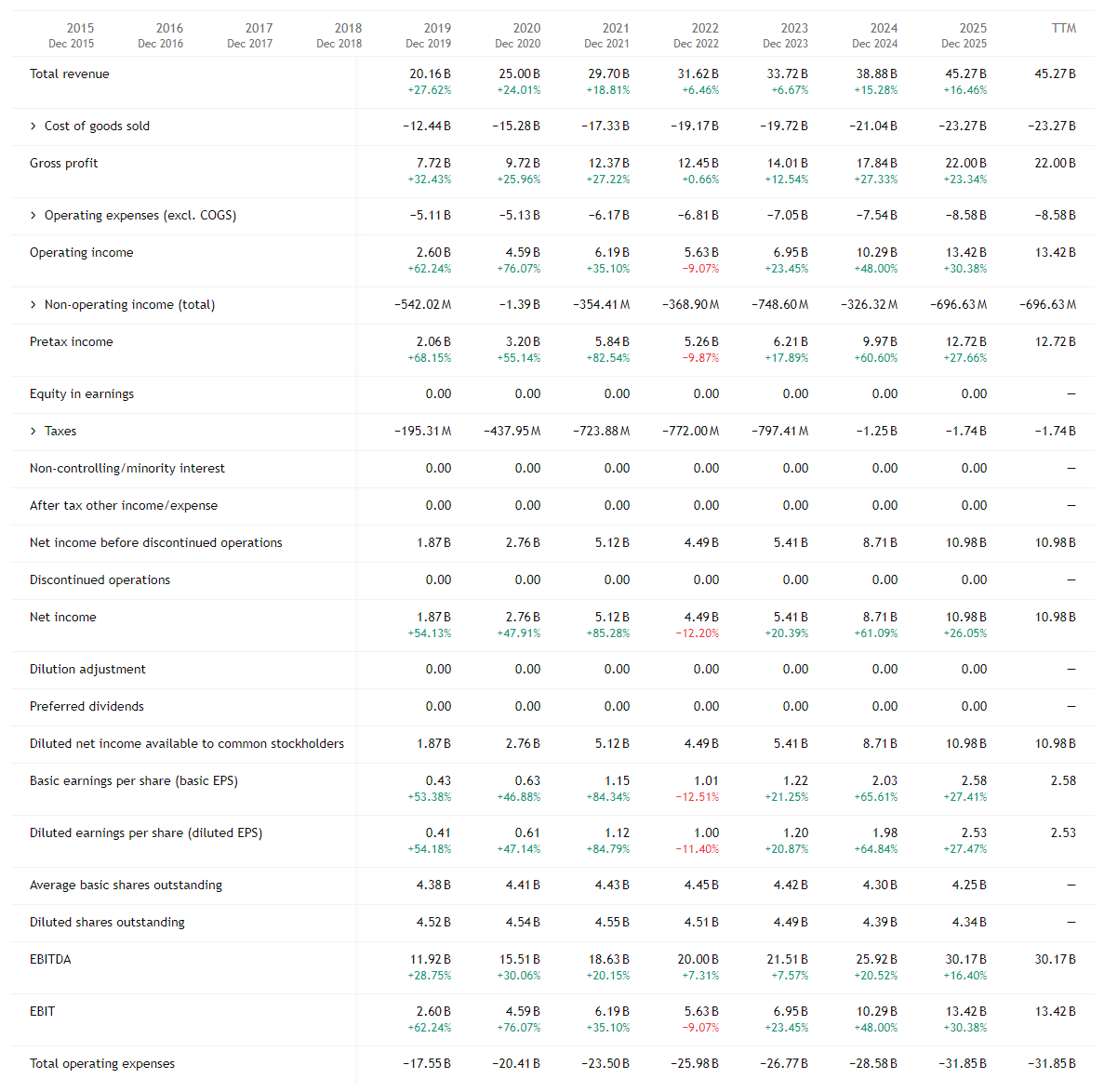

Netflix’s revenue grew from $6.8 billion in 2015 to $45.2 billion in 2025. That represents more than a sixfold increase over ten years, highlighting the power of its global subscription model.

From 2015 to 2021, the company experienced a period of rapid expansion. Revenue climbed from $6.8B to $29.7B, driven by international market entry, rising broadband penetration, original content investments, and strong subscriber additions. The 2020 to 2021 period saw an additional boost from pandemic-driven streaming demand, accelerating member growth and engagement.

However, growth moderated in 2022 and 2023. Revenue increased from $29.7B in 2021 to $31.6B in 2022 and $33.7B in 2023. While still positive, the pace slowed meaningfully. This period coincided with subscriber stagnation in mature markets, intensified competition, and a strategic reset as management introduced advertising and tightened password-sharing policies.

The slowdown proved temporary. In 2024 and 2025, revenue growth reaccelerated, reaching $39.0B and then $45.2B, respectively. This renewed momentum reflects improved monetization rather than pure subscriber expansion. Advertising revenue, paid sharing initiatives, and selective price increases helped lift average revenue per member while content spending became more disciplined.

Structural Evolution

The broader trend over the decade shows three distinct phases:

• High-growth global expansion

• Mid-cycle slowdown and recalibration

• Monetization-driven reacceleration

This evolution signals a shift from a purely subscriber-growth narrative to one centered on operating leverage, pricing power, and free cash flow generation.

Rather than plateauing after saturation fears in 2022, Netflix demonstrated the ability to adapt its model and unlock new revenue streams. The recent acceleration suggests the business is transitioning from a high-growth disruptor to a more mature, yet still expanding, global media platform.

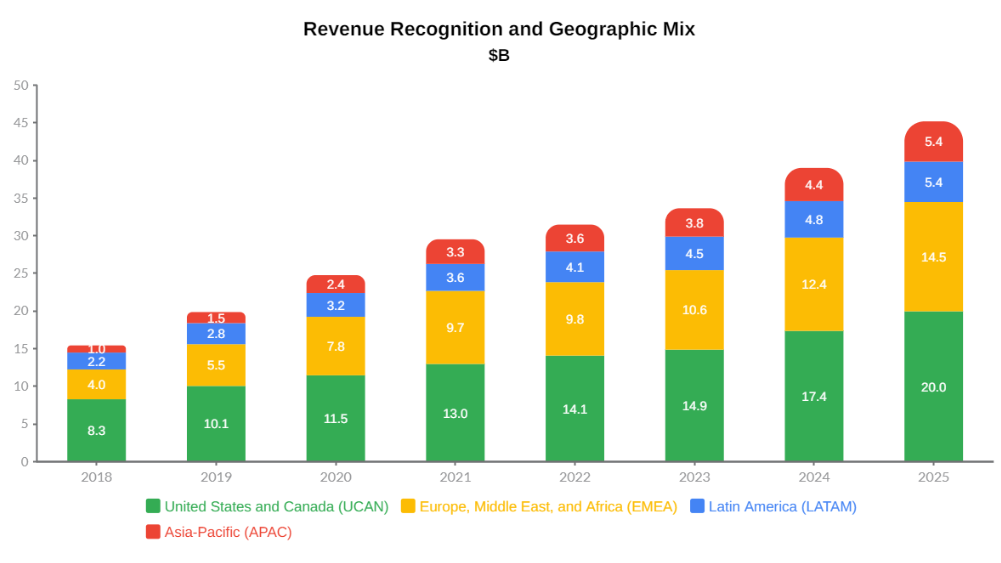

Revenue Recognition and Geographic Mix

Netflix primarily generates revenue from subscription streaming, recognized ratably over the period members receive access to the service. Because subscriptions are typically billed monthly, revenue is recorded over time rather than upfront. This creates a predictable, recurring revenue model tied directly to active memberships and pricing tiers.

Unlike traditional media companies that monetize individual titles, Netflix generates revenue from access to its entire platform. Members subscribe to the ecosystem rather than paying per show or film, reinforcing the portfolio-based nature of its business model.

For analytical clarity, this section focuses specifically on streaming revenues by region, not consolidated total revenues. In earlier years, Netflix also operated its legacy DVD-by-mail segment. Revenue from that business was included in the overall “Total Revenues” but was separate from “Total Streaming Revenues,” which reflects only the streaming business.

The difference in those years reflects the remaining contribution of the DVD segment. As that business declined and was ultimately wound down, streaming became the dominant driver of company revenue. By 2024 and 2025, total revenue and streaming revenue align at $39.0B and $45.2B, underscoring Netflix’s evolution into a fully streaming-driven global platform.

Geographic Revenue Breakdown

Netflix reports streaming revenue across four primary regions:

- United States and Canada (UCAN)

- Europe, Middle East, and Africa (EMEA)

- Latin America (LATAM)

- Asia-Pacific (APAC)

United States and Canada (UCAN)

Revenue grew from $8.3B in 2018 to $20.0B in 2025. UCAN remains Netflix’s largest and most profitable region. Growth here has shifted from rapid subscriber additions to monetization through pricing power, paid sharing, and advertising.

Europe, the Middle East, and Africa (EMEA)

EMEA expanded from $4.0B in 2018 to $14.5B in 2025. The region has become a major growth engine, supported by local-language content and strong adoption across Western Europe and emerging markets.

Latin America (LATAM)

LATAM revenue increased from $2.2B in 2018 to $5.4B in 2025. Growth has been steady but more moderate, reflecting pricing sensitivity and currency volatility.

Asia-Pacific (APAC)

APAC revenue rose from $1.0B in 2018 to $5.4B in 2025. While smaller in absolute size, this region has delivered some of the fastest percentage growth, driven by expanding broadband access and strong regional content performance.

The data highlights two major shifts:

- The evolution from a hybrid DVD + streaming company to a fully streaming-driven model.

- The transition from a U.S.-centric business to a globally diversified revenue base.

Today, Netflix’s revenue recognition is almost entirely subscription streaming-based, with international markets representing a substantial share of total revenue. The business has moved beyond early expansion and is now optimizing monetization across a broad global footprint.

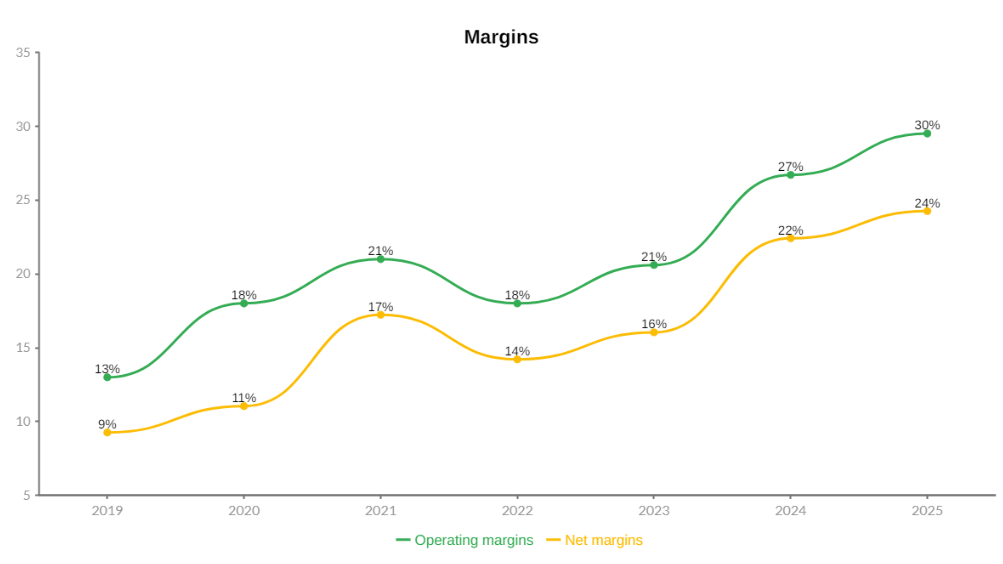

Margin Profile: Operating and Net Margins

The margin trajectory for Netflix from 2019 to 2025 highlights the company’s shift from aggressive expansion to disciplined, profitable scale.

Operating margin improved from 13% in 2019 to 30% in 2025. In the years leading up to 2021, margins expanded steadily, reaching 21% as subscriber growth and global expansion drove strong revenue gains. Because much of Netflix’s cost structure, particularly content amortization and technology infrastructure, benefits from scale, revenue growth outpaced operating expense growth during this period.

In 2022, operating margin dipped to 18%. This decline coincided with the well-documented subscriber slowdown and rising competitive pressures. It was a reminder that even scaled platforms are not immune to market resets. However, the contraction proved temporary. By 2023, margins began to recover, and by 2024 and 2025, operating margins reached 27% and then 30%, marking new highs. This expansion reflects improved monetization through pricing adjustments, paid sharing initiatives, advertising contributions, and tighter control over content spending.

Net margin followed a similar pattern, rising from 9% in 2019 to 24% in 2025. The dip in 2022 to 14% mirrors the operating margin compression that year, but the rebound was equally strong. The steady improvement in net margin suggests that interest expense and taxes have not materially eroded profitability gains. For a business with meaningful content investment and debt obligations, a mid-20% net margin indicates significant earnings power.

More broadly, margin expansion matters because it demonstrates operating leverage. Revenue growth alone tells us the platform is scaling; margin growth confirms that scale is translating into profitability. The post-2022 recovery suggests Netflix has entered a more mature phase of its lifecycle, where growth and efficiency are increasingly balanced. If sustained, a 30% operating margin combined with expanding net margins materially strengthens long-term earnings compounding potential.

📌 Further Reading

- Quarterly Earnings & Shareholder Letters

https://ir.netflix.net/financials/quarterly-earnings/default.aspx

Detailed quarterly financial results, margin updates, and forward-looking commentary. - SEC Filings (10-K, 10-Q)

https://www.sec.gov/edgar/browse/?CIK=1065280

Official regulatory filings containing audited financials, risk disclosures, and segment-level detail.

Media & Entertainment Industry Overview

The global media and entertainment industry encompasses businesses that create, produce, and distribute content across film, television, music, publishing, gaming, advertising, sports, and digital platforms. Between 2019 and 2025, the industry has undergone one of the most significant structural transformations in its history, driven by streaming adoption, mobile-first consumption, digital advertising growth, and evolving monetization models.

For the purposes of this thesis, growth rates referenced reflect compound annual growth rates unless otherwise specified.

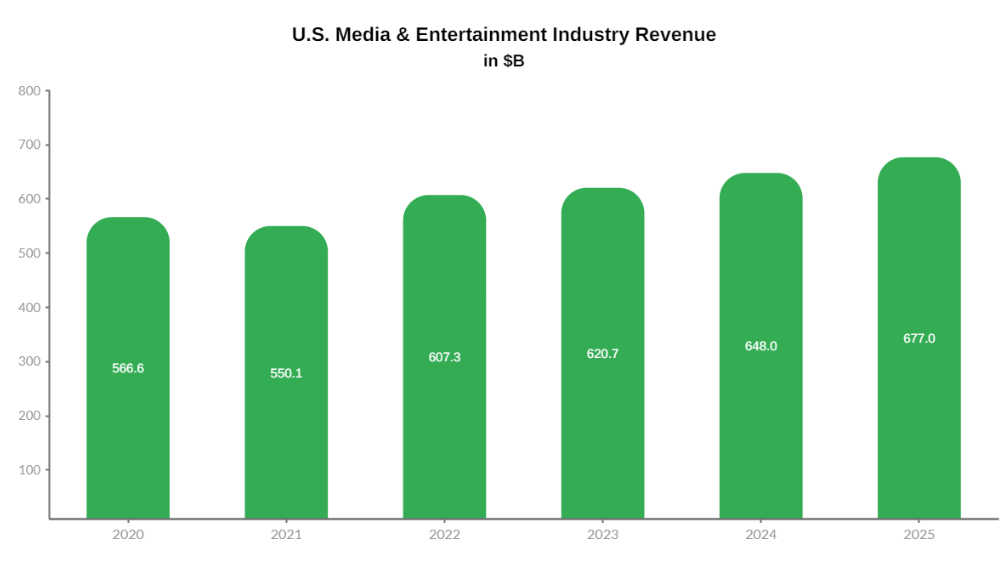

Industry Resilience and Structural Shift

From 2019 to 2023, the U.S. media and entertainment industry demonstrated notable resilience despite the pandemic-driven contraction of 2020. According to available industry research and market analyses, revenues declined by about 2.9% to $550.1 billion in 2020 before rebounding sharply by around 10.4% in 2021 to $607.3 billion. By 2023, revenues reached $620.7 billion and were projected, at the time of reporting, to rise to approximately $677 billion by 2025.

Importantly, this recovery was not merely cyclical. It coincided with an accelerated shift toward digital distribution and subscription-based models. Consumer and advertising spending grew to $562 billion in 2023 and was expected to exceed $620 billion by 2025, underscoring the sector’s economic durability and its reputation as relatively recession-resilient.

Digital media spending expanded from $177 billion in 2019 to $320 billion in 2023, growing at nearly 16% annually over that period. Digital channels officially surpassed traditional media spending in 2021 and are projected to represent roughly two-thirds of total industry spend by 2028.

This structural migration from traditional to digital formats forms the foundation of Netflix’s long-term opportunity.

The Shift to Streaming and OTT

Filmed entertainment remains the largest revenue contributor within the industry. However, the composition of that revenue has shifted meaningfully.

Spending on theatrical releases and traditional cable television has declined, while subscription video-on-demand (SVOD), ad-supported video-on-demand (AVOD), and transactional VOD have grown rapidly. Over-the-top (OTT) delivery is now the dominant distribution mechanism for professionally produced video content.

This transition directly benefits global streaming platforms such as Netflix. As consumer behavior shifts toward on-demand, internet-delivered video, streaming becomes not just a complementary channel but the primary mode of content consumption.

The pandemic accelerated this shift by several years. Even as theatrical attendance and live sports have gradually recovered, consumer habits have permanently changed. The living room is now powered by broadband, smart TVs, and mobile devices rather than cable bundles.

Sector Divergence: Digital Winners vs. Legacy Declines

Industry growth from 2019 to 2025 has been uneven across sectors.

Digital-native segments such as social media and video games captured double-digit growth rates, benefiting from scalable technology platforms and advertising monetization. Internet advertising, in particular, has become a central driver of industry economics.

Conversely, traditional print sectors including newspapers and magazines have experienced structural declines in revenue, profitability, and employment. Books have remained relatively stable but show limited growth compared to digital-first businesses.

Filmed entertainment occupies a hybrid position. While legacy distribution models have softened, digital streaming has supported overall expansion. The sector generated over $150 billion in revenue in 2023 and is projected to continue growing modestly through 2025.

For Netflix, this divergence is critical. The company operates within filmed entertainment but benefits from digital-first economics rather than legacy infrastructure.

Profitability and Industry Value Creation

Industry contribution to GDP, or industry value added, grew from $265 billion in 2019 to $304 billion in 2023 and was projected, at the time of reporting, to exceed $339 billion by 2025. Notably, profitability growth is projected to outpace revenue growth in the coming years.

Digital platforms tend to exhibit stronger scalability once fixed content and technology costs are absorbed. As streaming platforms mature, margin expansion becomes increasingly tied to pricing power, advertising monetization, and operating leverage.

This dynamic mirrors Netflix’s own margin trajectory. After a decade of aggressive global expansion and heavy content investment, the industry environment now favors cost discipline, advertising tier adoption, and monetization optimization rather than pure subscriber growth.

Employment and Economic Footprint

Industry employment recovered from pandemic lows and is projected to exceed 2.1 million jobs by 2025 in the United States alone. Job growth is concentrated in digital sectors, including streaming infrastructure, data analytics, advertising technology, and content production.

The labor mix is shifting toward technology-enabled roles, reflecting the platformization of entertainment. For Netflix, this reinforces its positioning not merely as a studio, but as a global technology-enabled media platform.

Global Context and Emerging Themes

Beyond the U.S., emerging markets such as Indonesia illustrate broader global trends:

- Rising internet penetration and mobile access

- Increasing digital literacy

- Rapid adoption of streaming services

- Growth in gaming, esports, and interactive media

- Government-supported digital infrastructure transitions

These trends expand the total addressable market for global streaming platforms. As broadband access improves and middle-class income rises, subscription streaming becomes more accessible to a larger global audience.

Additionally, generative AI is poised to reshape content creation, localization, personalization, and cost structures across the industry. While still early, AI may improve efficiency in dubbing, subtitling, recommendation algorithms, and production workflows, potentially enhancing long-term margin profiles for scalable platforms like Netflix.

Strategic Implications for Netflix

The media and entertainment industry between 2019 and 2025 is defined by three structural realities:

- Digital distribution has overtaken traditional channels.

- Subscription and advertising-based models are increasingly dominant.

- Profitability is shifting toward scalable, global platforms.

Netflix operates at the center of these transformations. As a pure-play global streaming platform, it is aligned with the fastest-growing segments of industry spend, benefits from digital scalability, and participates directly in the structural migration away from linear television.

Rather than competing within a shrinking legacy framework, Netflix is positioned within the industry’s long-term growth engine: global, internet-delivered, on-demand entertainment.

📌 Further Reading

- Protemus Media & Entertainment Industry Report

https://www.protemus.id/public/upload/industries/1698996889.pdf

Industry trends, M&A insights, and structural developments within the media ecosystem. - Pepperdine Institute for Entertainment, Media & Sports

https://digitalcommons.pepperdine.edu/

Academic research and capital market analysis on entertainment and media companies.

Competitive Landscape & Structural Positioning

Netflix as a Pure-Play Streaming Platform

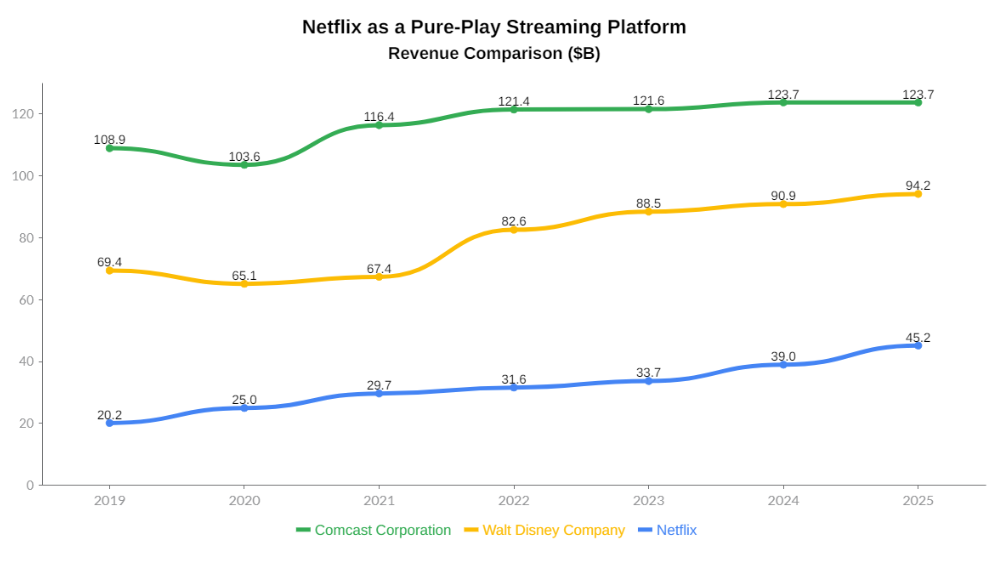

Netflix occupies a structurally distinct position within the competitive landscape: it is a pure-play, global streaming platform operating at meaningful scale, yet still smaller in total revenue than diversified incumbents such as The Walt Disney Company and Comcast Corporation.

In 2025, Netflix generated approximately $45 billion in revenue, compared to roughly $94 billion for Disney and $124 billion for Comcast. On absolute size, Netflix sits below both. However, the composition of that revenue tells a more important story than the headline numbers.

Revenue Concentration vs. Diversification

Disney’s revenue base spans theme parks, consumer products, linear television networks, film studios, and streaming services. Comcast combines broadband infrastructure, cable distribution, NBCUniversal media assets, and theme parks. Streaming, for both, is a strategic segment within a broader conglomerate structure.

Netflix, by contrast, generates almost all of its revenue from streaming subscriptions and, more recently, its advertising-supported tier. It does not rely on theme park attendance, broadband fees, hardware sales, or cloud computing to support its platform.

This concentration creates both limitation and strength. Netflix cannot subsidize streaming losses with unrelated profit pools. Yet it also avoids internal capital allocation conflicts and legacy drag from slower-growth divisions. Its financial performance reflects the economics of streaming directly and transparently.

Discipline and Platform Identity

Being a pure-play operator imposes operational discipline. Content investment, pricing increases, password-sharing enforcement, advertising rollout, and global expansion must each justify themselves economically. There is no external segment to absorb inefficiencies.

Over time, this structure has shaped Netflix into a highly data-driven, globally scaled distribution engine rather than a traditional studio. The company monetizes its content library continuously across markets, rather than relying on theatrical windows or physical distribution cycles.

Recent strategic moves reinforce this focus. Netflix has expanded its ad-supported tier, tightened paid sharing policies to boost monetization, raised prices selectively in mature markets, and continued investing in international originals to deepen global engagement. These initiatives aim to accelerate revenue growth and expand margins within the streaming model itself.

Can Netflix Close the Scale Gap?

While Netflix remains smaller in total revenue today, it operates almost entirely within the industry’s fastest-growing segment: digital, direct-to-consumer streaming.

For Netflix to surpass Disney over time, it would need sustained ARPU growth, successful advertising scale, and continued global subscriber expansion, alongside disciplined content spending. Surpassing Comcast would be more difficult given Comcast’s broadband infrastructure revenues, which provide stable, recurring cash flows outside of media.

The central investment question is therefore not current size, but trajectory. Netflix is structurally aligned with the long-term shift toward internet-delivered entertainment. If streaming continues gaining share from linear television and traditional distribution, a focused, asset-light global platform may narrow the revenue gap with diversified incumbents.

In a competitive field where many players treat streaming as one division among many, Netflix remains singularly defined by it. That clarity of purpose continues to anchor its strategic positioning.

Streaming in the Age of Tech Ecosystems

While Netflix competes directly for viewer attention and subscription dollars, its competition with large technology firms operates on a fundamentally different level. Companies such as Amazon, Apple Inc., and Alphabet Inc. approach streaming not as a standalone profit engine, but as one component within vast, multi-segment ecosystems.

This distinction matters. The comparison here is not about total company revenue. Amazon, Apple, and Alphabet generate the majority of their revenue from e-commerce, hardware, cloud services, and digital advertising. Streaming is strategically important, but financially integrated into much larger operating systems.

Amazon’s Prime Video supports and reinforces its broader Prime membership ecosystem, which drives retail loyalty and recurring subscription revenue. Apple TV+ strengthens customer retention across Apple’s hardware and services portfolio. Alphabet monetizes video primarily through YouTube, leveraging the world’s largest digital advertising infrastructure.

These firms possess structural advantages that differ from traditional media competitors. Their capital bases are significantly larger, allowing sustained investment in content without immediate profitability pressure. They benefit from cross-platform distribution across devices, operating systems, app stores, and cloud infrastructure. In Alphabet’s case, deep advertising technology capabilities create powerful monetization leverage across video inventory.

For Netflix, this creates a distinct competitive dynamic. It cannot rely on hardware integration, retail bundling, or search-based ad dominance to subsidize streaming. Its capital allocation must be justified within streaming economics alone.

However, that limitation also reinforces focus. Netflix’s singular objective is optimizing engagement, pricing power, content return on investment, and global subscriber growth. In contrast to Big Tech competitors, whose streaming services serve broader ecosystem goals, Netflix remains structurally aligned around streaming as the core product.

In this sense, competition with Big Tech is not a direct revenue contest, but a structural one. It pits a focused, global streaming platform against diversified technology ecosystems with cross-subsidy capabilities. Understanding that distinction is critical when evaluating Netflix’s competitive positioning and long-term scalability.

📌 Further Reading

- Alphabet Inc. (GOOGL)

https://www.gosnowballinvesting.com/google/

In-depth breakdown of Alphabet’s business model, advertising dominance, and platform economics. - Amazon.com, Inc. (AMZN)

https://www.gosnowballinvesting.com/amazon/

Analysis of Amazon’s ecosystem strategy, Prime flywheel, and long-term competitive advantages. - Apple Inc. (AAPL)

https://www.gosnowballinvesting.com/apple/

Deep dive into Apple’s services expansion, ecosystem integration, and long-term monetization strategy.

Leadership

Netflix’s evolution from DVD startup to global streaming leader has been shaped by long-term strategic thinking, disciplined execution, and a willingness to disrupt its own model. At the center of this transformation are three key leaders who represent different phases of the company’s development: Reed Hastings, who defined its culture and strategic pivots; Ted Sarandos, who built its global content engine; and Greg Peters, who is leading its monetization and platform optimization era.

Reed Hastings

Founder and Chairman

Reed Hastings co-founded Netflix in 1997 and served as CEO for 25 years, guiding the company through its most critical transitions. Under his leadership, Netflix shifted from DVD-by-mail to streaming in 2007, a decision that redefined the company’s trajectory and positioned it ahead of industry disruption.

He championed the subscription model, eliminated late fees, and embedded data-driven personalization into the product early on. The recommendation system introduced in the DVD era later became foundational to Netflix’s streaming advantage. Hastings also drove the move into original content beginning in 2013, reducing reliance on third-party studios and establishing Netflix as a global studio.

Equally important was the culture he institutionalized. The Netflix Culture Deck emphasized high performance, freedom with responsibility, and candid feedback. This operating philosophy enabled rapid decision-making and strategic boldness during pivotal moments, including international expansion, content investment scaling, and the 2022 reset toward monetization and profitability.

Ted Sarandos

Co-CEO

Ted Sarandos has led Netflix’s content operations since 2000 and has been central to transforming the company into a global content powerhouse. He spearheaded the shift into original programming in 2013 with series such as House of Cards, Arrested Development, and Orange Is the New Black, establishing Netflix as a credible studio rather than just a distributor.

Under his leadership, Netflix scaled original production across genres and geographies, producing global hits including Stranger Things, La Casa de Papel, and Squid Game. The strategy of commissioning local-language content with global appeal became a core competitive advantage.

Sarandos also expanded Netflix’s creative footprint beyond traditional series and film into live programming, stand-up specials, sports-adjacent events, and theatrical experiences. His focus on talent relationships and long-term content investment has reinforced Netflix’s position as a first-choice platform for creators worldwide.

Greg Peters

Co-CEO

Greg Peters represents the platform and monetization phase of Netflix’s evolution. After serving in product, operations, and international leadership roles, he became co-CEO in 2023 during a period of strategic recalibration.

Peters has played a central role in launching the ad-supported tier, implementing paid sharing initiatives, and improving pricing architecture across global markets. These initiatives marked a shift from pure subscriber growth toward revenue optimization and margin expansion.

He has also overseen product innovation, including enhanced personalization features, mobile engagement tools, gaming integration, and improvements to the TV interface. Under his leadership, Netflix expanded into live programming at scale, including major sporting events and global broadcasts, while maintaining platform reliability.

In the 2023 to 2025 period, Peters’ focus on operational discipline, engagement-driven monetization, and scalable infrastructure has helped transition Netflix into a more mature, cash-generative business without compromising its growth ambitions.

Beyond these three leaders, Netflix’s executive bench adds further depth across finance, product, advertising, and global content. Spencer Neumann has strengthened capital discipline and free cash flow generation as Chief Financial Officer, supporting the company’s shift toward sustained profitability. Bela Bajaria oversees global content strategy, scaling local-language production into worldwide hits. Amy Reinhard leads the advertising business, building what is now a meaningful second revenue stream. Elizabeth Stone drives product and technology innovation, ensuring the platform remains scalable, personalized, and resilient as engagement expands into live programming and games.

Together, this leadership structure reflects a company that is no longer defined by a single strategic bet, but by coordinated execution across content, technology, monetization, and capital allocation. Netflix’s leadership evolution mirrors its business evolution: from disruption, to scale, to a disciplined global platform.

📌 Further Reading

- Netflix Leadership Team

https://about.netflix.com/en/leadership

Executive biographies and organizational structure. - 2025 Proxy Statement

https://s22.q4cdn.com/959853165/files/doc_financials/2024/ar/Netflix-Inc-2025-Proxy-Statement.pdf

Executive compensation structure, governance practices, and shareholder voting matters.

Executive Compensation

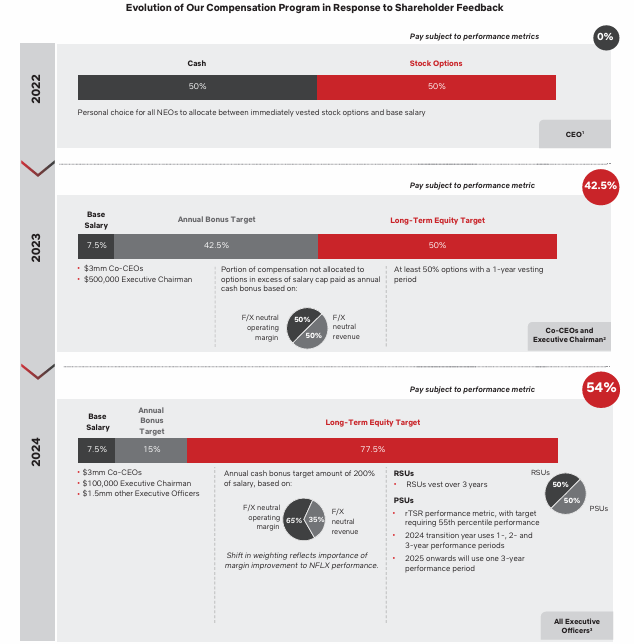

Evolution of the Compensation Structure

The visual above illustrates how Netflix has redesigned its executive compensation framework from 2022 through 2024 in response to investor feedback and a broader shift toward performance alignment.

In 2022, executive compensation was split evenly between cash and stock options, with flexibility for certain leaders to allocate between salary and immediately vested equity. Notably, 0% of target pay was formally tied to structured performance metrics. While equity exposure aligned executives with shareholders, compensation was not explicitly linked to margin or revenue thresholds.

In 2023, Netflix introduced performance-based accountability into the framework. Approximately 42.5% of target pay became subject to financial metrics, including operating margin and revenue. The structure combined base salary, annual bonus targets, and long-term equity, with at least 50% of equity subject to structured vesting.

By 2024, the model further strengthened. Roughly 54% of target compensation became performance-based, and long-term equity weighting increased to as much as 77.5% of total target pay. Performance stock units incorporated multi-year measurement periods, and metric weighting increasingly emphasized margin expansion. This evolution mirrors Netflix’s strategic shift from subscriber hypergrowth toward monetization discipline, operating leverage, and free cash flow generation.

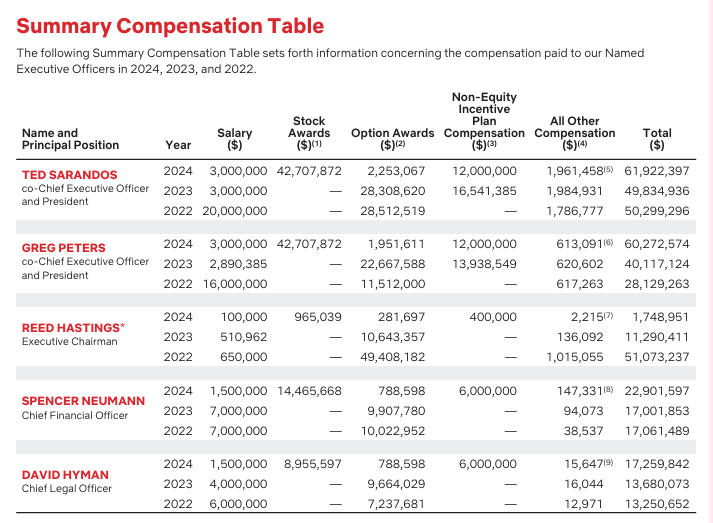

Summary Compensation Table

The summary compensation table provides the realized compensation for Named Executive Officers from 2022 through 2024, reflecting how the structural changes translated into actual pay outcomes.

For 2024, Co-CEOs Ted Sarandos and Greg Peters each received $3 million in base salary, but total compensation exceeded $60 million for both, driven primarily by stock awards, option awards, and performance-based incentives. The majority of their compensation is therefore variable and equity-linked rather than fixed salary. This structure reinforces long-term shareholder alignment, as realized value depends significantly on stock performance and achievement of financial targets.

Non-equity incentive plan compensation also reflects performance linkage. In 2024, both Co-CEOs received $12 million in incentive compensation, while CFO Spencer Neumann received $6 million. These payouts suggest that key financial targets tied to operating margin and revenue were achieved during the year.

Reed Hastings’ compensation profile reflects his transition to Executive Chairman. By 2024, his total compensation was substantially lower than during his tenure as CEO, consistent with a governance-focused role rather than operational leadership.

Across executives, year-to-year variability in total compensation is largely driven by equity award timing and stock-based compensation structures. This variability is typical for performance-aligned models and underscores the linkage between executive wealth creation and shareholder returns.

Taken together, both the structural evolution and the compensation outcomes demonstrate a clear trajectory: Netflix has moved toward a majority performance-based, equity-heavy compensation framework aligned with operating margin expansion, revenue growth, and long-term value creation.

Risks

Investing in Netflix comes with several material risks that could impact growth, profitability, and shareholder returns.

Subscriber Growth and Retention Risk

Netflix’s business depends on continuously attracting and retaining members. Growth can slow in mature markets, and competition for consumer attention is intense. Members may cancel due to pricing changes, dissatisfaction with content, economic pressures, or better alternatives. Because content costs are largely fixed and committed in advance, slower growth could pressure margins and cash flow.

Intense Competition

The streaming market is highly competitive, with rivals ranging from traditional broadcasters and studios to global tech platforms, gaming companies, and even piracy services. Competitors may offer exclusive content, bundle services, or price aggressively. Rapid technological change, including advancements in generative AI, could also shift competitive dynamics.

Content and Production Risk

Netflix invests billions in licensed and original programming. Not all content succeeds, and misjudging audience preferences can lead to weaker engagement and lower returns on investment. Production delays, labor disputes, rising talent costs, or intellectual property disputes could increase expenses or disrupt releases. Content licensing negotiations may also become more costly or restrictive over time.

Regulatory and Reputation Risk

Operating in over 190 countries exposes Netflix to varying regulatory environments, censorship requirements, tax regimes, and local content quotas. Changes in data privacy laws, advertising regulations, or internet policies such as net neutrality could increase costs or limit flexibility. Controversial content, advertising backlash, or ESG-related scrutiny could harm the brand and trigger regulatory responses.

Technology and Cybersecurity Risk

Netflix relies heavily on cloud infrastructure, including Amazon Web Services, content delivery networks, and third-party payment systems. System failures, cyberattacks, data breaches, or service disruptions could damage its reputation and lead to financial and regulatory consequences. As a high-profile digital platform, it remains an attractive target for cybersecurity threats.

Financial and Liquidity Risk

Netflix carries significant long-term content obligations and debt. As of the latest reporting period, it had billions in senior notes and substantial content liabilities. Because many content commitments are fixed and multi-year in nature, the company has limited flexibility to quickly reduce costs if growth slows. Rising interest rates, refinancing risks, or large acquisitions could further pressure liquidity and balance sheet strength.

International and Currency Risk

A meaningful portion of revenue comes from outside the United States. Currency fluctuations, inflation, geopolitical instability, tax changes, or local regulatory shifts could impact reported earnings and operational stability.

Advertising Execution Risk

Netflix’s advertising-supported tier is still relatively new. Advertising revenue depends on member engagement, advertiser demand, regulatory developments, measurement capabilities, and competition for ad budgets. Execution missteps or advertiser pullbacks could limit expected upside from this segment.

Stock Price Volatility

Netflix’s stock has historically been volatile. Results can fluctuate due to membership trends, content performance, competitive developments, macroeconomic factors, or shifts in investor expectations. Forecasting subscriber growth, advertising adoption, and new initiatives carries inherent uncertainty, and deviations from expectations could lead to sharp market reactions.

Why Netflix Remains a Compelling Long-Term Investment

Netflix today is not the same company it was during its hypergrowth phase. It has evolved from a disruptive streaming pioneer into a scaled, cash-generative global entertainment platform with expanding margins and diversified monetization levers.

Structurally, Netflix remains uniquely positioned. As a pure-play streaming platform, its entire organization is aligned around one objective: optimizing engagement, pricing power, and global content distribution. Unlike diversified media conglomerates or Big Tech ecosystems where streaming is one segment among many, Netflix’s focus reinforces clarity in capital allocation and strategic execution.

Financially, the company has entered a new phase. The shift toward paid sharing enforcement, the expansion of its advertising-supported tier, and disciplined content investment have improved operating margins and strengthened free cash flow generation. Executive compensation has also evolved to emphasize performance-based metrics and long-term equity alignment, reinforcing accountability to shareholders.

Strategically, Netflix continues to extend its platform. Global local-language content production, entry into live programming, selective sports rights, gaming integration, and product enhancements deepen engagement and expand monetization opportunities without fundamentally altering the subscription-first model. Membership scale, now exceeding 300 million, provides both pricing leverage and advertising optionality.

Importantly, Netflix operates in the industry’s long-term growth lane: direct-to-consumer, internet-delivered entertainment. While competition remains intense, the company’s global scale, data-driven personalization engine, content flywheel, and disciplined cost structure create durable competitive advantages.

For long-term investors, Netflix represents a rare combination: a category-defining brand, global platform scale, improving profitability, and multiple monetization pathways. Its transition from growth-at-all-costs to margin-focused expansion strengthens the investment case, positioning the company to compound value over time rather than simply chase subscriber numbers.

In short, Netflix is no longer just a streaming disruptor. It is a mature, strategically aligned platform built for durable, long-term value creation.

📌 Build Your Snowball

🔗 Explore our long-term investment philosophy at Snowball Investing.

🔗 Discover how Netflix can anchor durable portfolio growth in The Essentials of Snowball Investing.

🔗 Browse our curated list of top investing book recommendations.

🎧 Listen to the Snowball Investing Podcast for audio versions of our featured insights.

The following data snapshots are as of 2/26/2025 from tradingview website

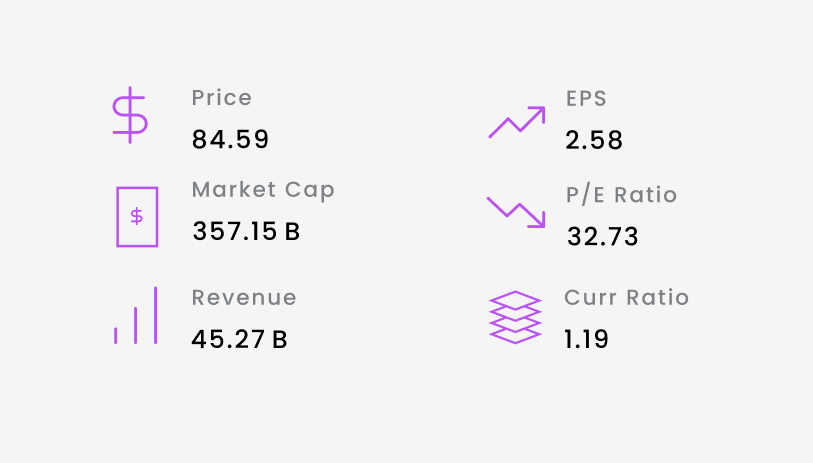

Key Stats

Performance since IPO

Financial Statements

Income Statement

Balance Sheet

Cash Flow

Statistics

Sources: Netflix

Unlock the power of compounding

We are changing the way that people build wealth. If your portfolio is performing below S&P 500 in the last 5 years, then you need to subscribe here. Discover remarkable stories directly to your inbox. As a subscriber, you'll receive the valuable recommendation of an exceptionally outstanding company that are designed to help you build wealth.

Gain access to exclusive benefits by subscribing today!

Disclaimer: Please note that this newsletter is a financial information publisher and not an

investment advisor. Subscribers should not view this newsletter as offering personalized legal or investment

counseling. Investors should consult with their investment advisor and review the prospectus or financial / stock

recommendation of the issuer in question before making any investment decisions. All articles, blogs, comments,

emails, and chatroom contributions - even those including the word "recommendation" - should never be construed as

official business recommendations or advice. Liability of all investment decisions resides with the individual

investor.

Snowball Investing does not provide any guarantees, warranties, or representations, whether explicitly or

implicitly, regarding the accuracy, reliability, completeness, or reasonableness of the information presented. The

opinions, assumptions, and estimates expressed represent the author's viewpoints as of the publication date and are

subject to modification without prior notification. Projections made within the document are based on various market

condition assumptions, and there is no assurance that the anticipated results will be attained. Snowball Investing

disclaims any responsibility for losses incurred due to reliance on this document's content. It is important to note

that Snowball Investing is not offering financial, legal, accounting, tax, or other professional advice, nor is it

assuming a fiduciary role.

Member discussion